Class Action Lawsuit Again a Foreign Company

Introduction

Companies headquartered or with principal places of business concern outside the United States ("non-U.Southward. issuers") go on to be targets of securities class deportment filed in the United States. Indeed, 2022 continued to see an uptick in the number of securities class activity lawsuits brought against not-U.S. issuers from the previous year, consistent with the general trend of filings trending upwards over the last decade. It is therefore imperative that multinational companies non simply pay attention to contempo filing trends in the United states of america, just that they also accept proactive measures to mitigate any potential risks.

In 2019, plaintiffs filed a full of 64 securities class activity lawsuits (as compared to 54 in 2018) against non-U.S. issuers through a total of 83 securities class activeness complaints filed before consolidation:

- The Second Circuit connected to exist the jurisdiction of choice for plaintiffs, with the next about popular circuit as the Third Circuit.

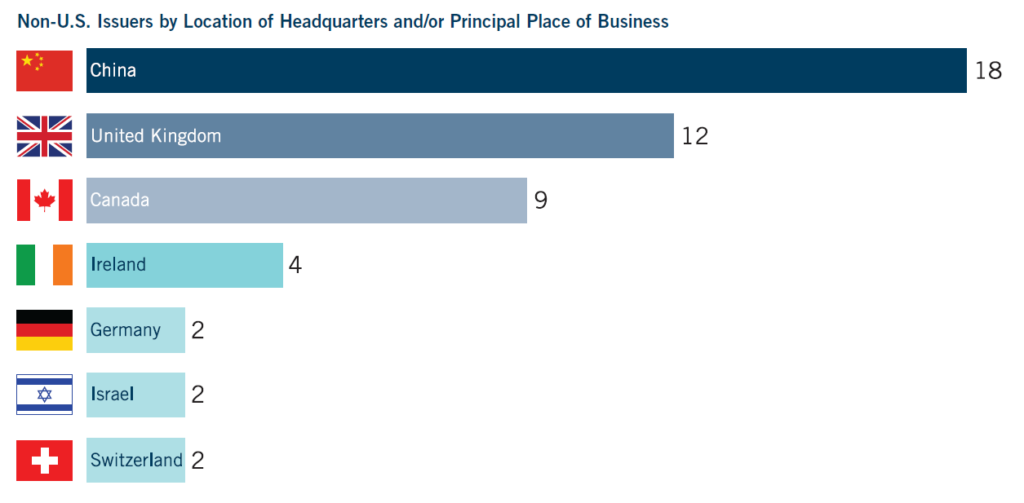

- Of the 64 non-U.Due south. issuers against whom securities form action complaints were filed in 2019, xviii have a headquarters and/or principal place of business in the People's Republic of China ("China"), 12 in the United Kingdom, and nine have corporate headquarters and/or master places of business in Canada.

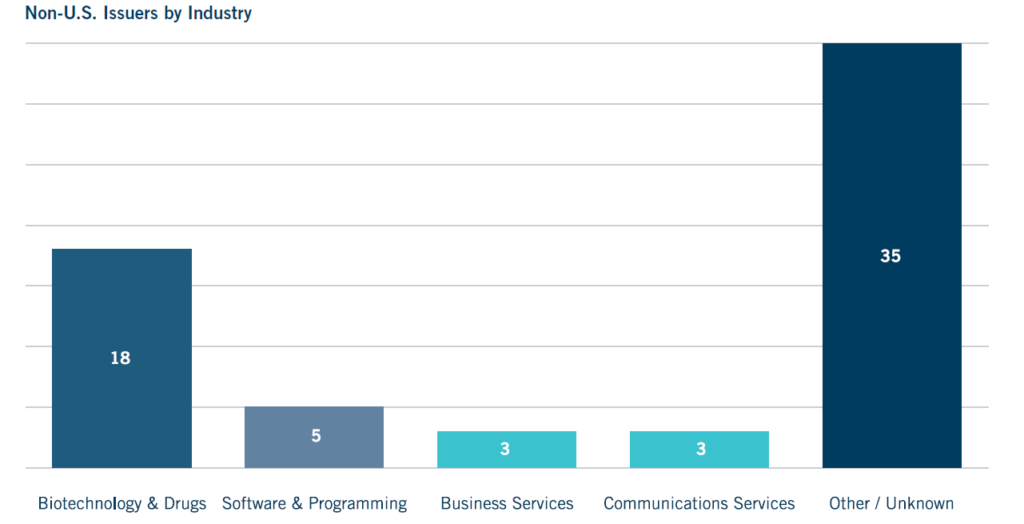

- The biotechnology and drugs industry was the manufacture with the largest number of class activeness lawsuits brought against non-U.S. issuers with 18 filed in 2019.

- The Rosen Law House P.A. connected to be the about agile law firm in this space, leading the style with respect to first-in-court filings against non-U.Southward. issuers in 2022 and with respect to the number of cases in which information technology was appointed every bit lead counsel.

An examination of the types of cases filed against non-U.Southward. issuers in 2022 reveals the post-obit substantive trends that were notable and specific to this year:

- Six of the non-U.S. issuers against whom securities course actions were filed in 2022 are alleged to take misrepresented the prospects of approving past the U.S. Nutrient and Drug Administration ("FDA") and/or compliance with FDA rules and regulations.

- Iii of the non-U.S. issuers against whom securities form actions were filed in 2022 are alleged to have failed to disclose alleged violations of Chinese government regulations.

- Three of the securities class actions filed confronting not-U.Due south. issuers in 2022 related to alleged bribery schemes.

- Seven of the non-U.Due south. issuers against whom securities class actions were filed in 2022 are alleged to have failed to disclose conflicts of interest that were purportedly relevant to investors.

In addition to these filings, in 2019, the U.S. Supreme Court too denied certiorari in the closely watched Toshiba affair, resulting in the Central District of California denying the newly filed move to dismiss. As discussed herein, this was an of import decision for non-U.S. issuers with unsponsored American Depositary Receipts ("ADRs").

Further, courts in 2022 and early on 2022 issued fewer dispositive decisions on motions to dismiss in securities course activity lawsuits brought against non-U.S. issuers than were issued in 2022 and early 2019. Specifically, merely seven dispositive motions to dismiss decisions were rendered with respect to securities grade actions that were initiated in 2018.

In addition, four 2022 filings were voluntarily dismissed in their entirety while ane 2022 filing was dismissed in its entirety pursuant to a stipulation between the parties. In that location were no dispositive motions to dismiss decisions rendered with respect to 2022 filings, but viii 2022 filings were voluntarily dismissed in their entirety, and i 2022 filing was dismissed in its entirety pursuant to a stipulation between the parties.

Although it is difficult to discern trends from just seven dispositive decisions, the courts' reasoning for dismissing cases—discussed below—is still instructive for not-U.S. issuers who may discover themselves bailiwick to securities class actions.

Not-U.S. Companies Remain Popular Targets for Securities Fraud Litigation

2019 saw an uptick in the number of securities course actions filed against non-U.S. issuers. This survey is intended to provide an overview of securities lawsuits confronting such companies. First, we analyze the number of cases filed, including trends relating to location of the courts, types of companies that are targeted and counsel retained. Side by side, nosotros analyze the dispositive securities decisions rendered against non-U.Southward. issuers in 2022 and early 2022 in an effort to provide insight to non-U.South. issuers who may observe themselves subject to securities class actions.

Filing Trends

In 2019, 404 securities course action lawsuits were brought with an increment over the previous year. Merely over 15% (64 of 404) of the class action lawsuits that were brought in 2022 were brought against non-U.S. issuers, a slight uptick from 2022 when 54 form actions lawsuits were brought against non-U.S. issuers. These course action lawsuits were initiated through 83 securities class action complaints. Every bit in years by, certain filing trends emerged:

- The Second Circuit continued to be the jurisdiction of pick for plaintiffs in 2019. More than 70% of the original 83 class action complaints (59) were initially filed in the Second Excursion with 41 of those filed in the Southern District of New York. The next most popular circuit was the Third Excursion, with 15 lawsuits initiated there. The Ninth Circuit saw five initial complaints and the Eleventh and Fifth Circuits followed, with 2 initial complaints each.

- Of the 64 non-U.S. issuers against whom securities class action complaints were filed in 2019, 18 have corporate headquarters and/or master places of business in China. Of these 18 companies, xv are incorporated in the Cayman Islands. None appear to be incorporated in Communist china.

- Twelve of the non-U.S. issuers against whom securities class actions were filed in 2022 have corporate headquarters and/or chief places of business in the United Kingdom. Nine have corporate headquarters and/or principal places of concern in Canada.

- With the legalization of recreational marijuana in Canada, six of the Canadian companies against whom securities class actions were brought in 2022 were cannabis- related companies.

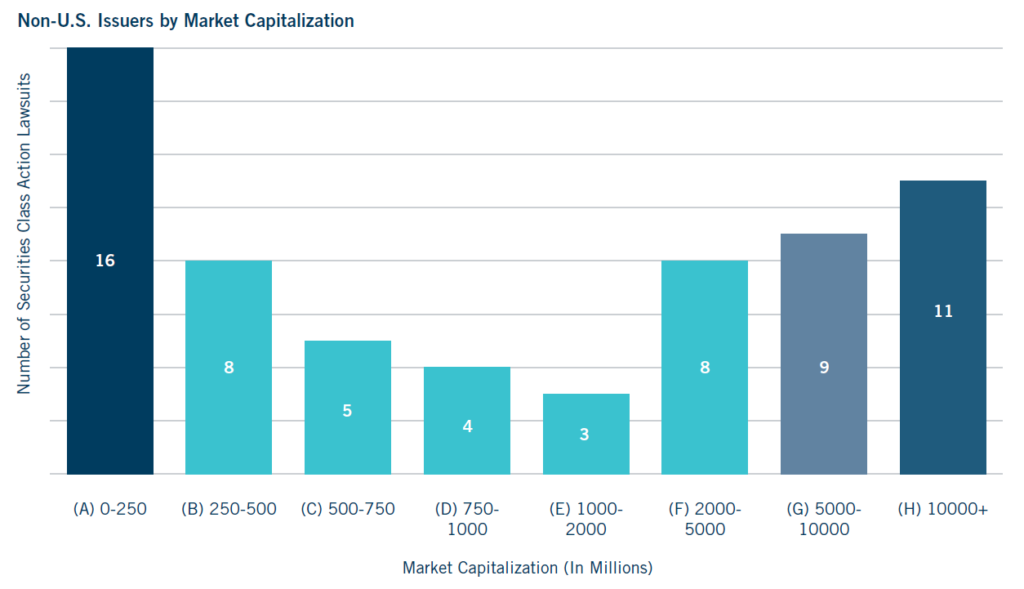

- The market capitalization of the non-U.S. issuers at the time at which the securities class actions were filed largely consisted of both smaller marketplace cap companies (16 of 64) nether U.s.a.$250 1000000 and larger market place cap companies (20 of 64) over US$5 billion.

- The biotechnology and drugs industry was the industry with the largest number of class activity lawsuits, with 18 filed in 2022 against not-U.S. issuers.

- As in 2018, the Rosen Law Firm P.A. continued to exist the most active constabulary business firm in this space. It led the way with respect to the number of first-in-court filings against non-U.Due south. issuers in 2022 (20) and with respect to the number of cases in which it was appointed as pb counsel (13).

- Also as in 2018, Pomerantz LLP and Glancy Prongay & Murray LLP followed with respect to first-in-court filings. Specifically, Pomerantz LLP was associated with 12 first-in-court filings, whereas Glancy Prongay & Murray LLP was associated with seven offset-in-court filings. With respect to lead counsel, Levi & Korsinsky, LLP followed the Rosen Police Firm P.A. and was appointed as pb counsel in seven cases while Pomerantz LLP and Robbins Geller Rudman & Dowd LLP were appointed as lead counsel in six cases each.

Substantive Trends

An examination of the types of cases filed in 2022 reveals iv notable trends this year in securities form actions brought against non-U.S. issuers. Specifically, companies are alleged to have:

- misrepresented the prospects of FDA blessing and/or compliance with FDA rules and regulations;

- failed to disclose declared violations of Chinese regime regulations;

- engaged in bribery; and

- failed to disclose conflicts of interest that were relevant to investors.

Cases Involving FDA Compliance

In 2019, the industry in which the largest number of securities class actions were filed against not-U.S. issuers was the biotechnology and drugs manufacture, with 18 of 64 securities class action suits filed. Several of the complaints against these companies involved allegations that defendants misrepresented the prospects of approval in the The states by the FDA and/or compliance with FDA rules and regulations. 2 such cases were filed in the District of New Jersey, where the multinational companies had U.S. operations. In In re Travis Ito-Stone, et al. v. DBV Technologies S.A., et al.,17 investors brought accommodate confronting accused DBV, a pharmaceutical company incorporated and headquartered in France with N American operations based in New Jersey, which supported the company'south manufacturing needs in North America. DBV trades on the National Clan of Securities Dealers Automatic Quotations Arrangement ("NASDAQ"). The company allegedly failed to disembalm serious manufacturing and quality control bug with its proposed peanut allergy handling. These problems allegedly threatened the production'due south prospects of obtaining FDA blessing in the United States of DBV's Biologics License Application and ultimately acquired DBV to withdraw its awarding. In re Amarin Corporation plc Securities Litigation involves allegations that defendant Amarin, headquartered in Ireland with a U.S. function in New Jersey, disclosed positive results from its clinical trials aimed at showing that the drug Vascepa could be used to reduce the risk of cardiovascular events, while failing to disclose 2 key issues with the results related to (1) the ceremoniousness of the placebo used, and (ii) the drug's causal mechanism. The plaintiffs allege that Amarin and its officers and directors, understood that those bug were significant to the scientific customs, investors and the public and that they could impact Vascepa's prospects for FDA approval.

Other cases involving alleged misrepresentations of FDA approving prospects were filed in the Southern District of New York, presumably because the companies trade on exchanges located within the district. For case, in Larry Enriquez, et al. v. Nabriva Therapeutics plc, et al., the plaintiffs criminate that Irish gaelic defendant Nabriva, which trades mutual stock on the NASDAQ, led the market to believe that FDA approval for a drug called Contepo was imminent and failed to disclose serious manufacturing problems that eventually led the FDA to reject to approve the Contepo New Drug Application ("NDA") also as a meaning filibuster in the drug's potential approval timeline. The disclosure of the FDA's refusal on April twenty, 2022 led to a 27% decline in Nabriva's share cost by market close on May 1, 2019. Also, in Josh Feierstein, et al. five. Correvio Pharma Corporation, et al., the plaintiffs criminate that the Canadian pharmaceutical company, Correvio (which trades on the NASDAQ), failed to disclose that the data supporting the resubmitted NDA for a treatment for the rapid conversion of contempo onset atrial fibrillation ("AFib") to sinus rhythm did not minimize the significant wellness and safety problems observed in connection with the drug's original NDA (namely, the death of a patient with AFib), which substantially macerated the likelihood of FDA approving.

Finally, in Daniel Brody, et al. five. Mylan N.5., et al.,22 investors filed in the Western District of Pennsylvania and allege that Dutch pharmaceutical company Mylan, with facilities in Pennsylvania, failed to disclose violations of FDA regulations at its' Morgantown, Due west Virginia manufacturing facility and that the company lacked effective internal control over financial reporting. As a result, the complaint alleges that upon the announcement of a restructuring and remediation program at Mylan's Morgantown facility, the stock cost dropped about 6.68%. The stock cost dropped an additional 15.06% and later 23.81% purportedly upon further announcements of financial results.

Cases Involving a Failure to Disclose Alleged Violations of Chinese Government Regulations

Of the 64 not-U.S. issuers against whom securities form actions were filed in 2019, 18 have corporate headquarters and/or principal places of business in China. Some of the not-U.Due south. issuers against whom securities class deportment were filed in 2022 allegedly failed to disclose violations or potential violations of Chinese regime regulations, the U.South. nexus for these cases being that the companies traded American Depository Shares ("ADSs") on the New York Stock Commutation ("NYSE") or NASDAQ. For example, in Theresa Gordon, et al. v. Tencent Music Entertainment Group, et al., the plaintiffs sued Tencent Music Amusement Group—an operator of online music amusement platforms that is headquartered in China, incorporated in the Cayman Islands, and trades ADSs on the NYSE. Investors allege that the registration argument and prospectus that Tencent had filed in connection with its IPO in late 2022 failed to disclose and/or made materially false and/or misleading statements regarding the anti-competitive efforts in which it was engaged and that such efforts "were reasonably likely" to result in Chinese regulatory scrutiny. Specifically, in these filings, Tencent allegedly failed to disembalm that its exclusive licensing agreements with record labels were anti-competitive and that that due to the anti-competitive nature of those licensing agreements, sublicensing content from Tencent was "unreasonably expensive"—a violation of Chinese antimonopoly laws. The plaintiffs further allege that when the anti-competitive nature of these agreements came to light on August 27, 2019, the price of Tencent's ADSs barbarous by 6.viii%.

Investors likewise filed arrange confronting Momo Inc., an operator of "several mobile-based social and entertainment platforms" in China. The plaintiffs allege that in 2014, the Chinese regime institute that Momo was a "purveyor" of pornographic content and that, in 2015, it fined the company. In add-on, the Chinese government allegedly ordered the company to "close down all pages that featured pornographic media, screen all media for pornography[,] temporarily arrive impossible for users to upload media[,] submit a rectification written report and make a public apology." The plaintiffs allege that in an effort to demonstrate to investors that it was no longer engaged in illicit activities, Momo—in its Securities and Exchange Commission ("SEC") filings—claimed that it was engaged in extensive content moderation to filter out indecent content. But the plaintiffs criminate that the reality was different. For example, the plaintiffs claim that a mobile dating application that Momo had acquired in 2022 was used to facilitate prostitution. When a announcer brought the alleged prostitution to lite, the Chinese regime allegedly took action, which included removing the application from Android phones and from Apple's App Shop. The plaintiffs allege that the disclosure and subsequent action caused Momo's stock toll to fall, damaging investors. The plaintiffs further allege that Momo failed to disclose in its SEC filings its relationship—and the resulting take a chance of exposure to Chinese regime regulation—with a talent agency that Momo allegedly used to find live performers (the majority of whom were allegedly "young attractive women"). When a tertiary-party annotator disclosed this relationship, Momo's stock price fell, allegedly further dissentious investors.

Cases Involving Bribery

Not-U.Southward. issuers can also be the bailiwick of securities class actions arising out of alleged or admitted blackmail schemes occurring inside and/or outside of the U.s.a.. Such cases were filed against iii companies in 2019. In Shayan Salim, et al. v. Mobile TeleSystems PJSC, et al., the plaintiffs allege that Russian telecommunications company Telesystems defrauded investors past issuing fake and misleading statements about the company'due south liability for an illegal blackmail scheme involving payments by a subsidiary for the benefit of an Uzbek regime official in gild to enter and operate in the Uzbek telecommunication marketplace between 2004 and 2012; the effectiveness of the company's internal controls and compliance; and the company's cooperation with a United States Strange Corrupt Practices Act investigation, which led to a deferred prosecution agreement that was unsealed in March 2019. The stock price allegedly barbarous approximately 8% on November 20, 2022 later on the magnitude of the company's potential liability to the SEC and the U.Southward. Department of Justice ("DOJ") for the bribery scheme was disclosed. The stock toll allegedly dropped an additional 3% on March 7, 2019, when the Deferred Prosecution Understanding with the DOJ was unsealed.

In Jung Kyoon Kong, et al. five. Fiat Chrysler Automobiles N.5., et al., as well filed in the Eastern District of New York, the plaintiffs allege that Fiat fabricated imitation and misleading statements in its SEC Form 20-F filings by failing to disembalm a bribery scheme that the company engaged in in lodge to obtain favorable terms in its commonage bargaining agreement with International Union, United Automobile, Aerospace and Agricultural Implement Workers of America. According to the complaint, the details of the bribery scheme began to emerge on November 20, 2019, when Full general Motors filed a racketeering lawsuit against Fiat, which purportedly acquired the stock toll to drop.

In William Likas, et al. five. ChinaCache International Holdings Express, et al., which is pending in the Primal District of California, plaintiffs claim that ChinaCache, a Chinese Company incorporated in the Cayman Islands and which trades ADRs on the NASDAQ, fabricated materially simulated and misleading statements past declining to disembalm that ChinaCache and the company'south Chief Executive Officer and Chairman of the Board of Directors were engaged in enterprise bribery. Details of the bribery scheme are non alleged. Upon the announcement, on May 17, 2019, of a criminal investigation into the bribery scheme in China, as well equally the CEO's arrest and resignation, the company'south stock cost allegedly fell 20%. A few days afterwards, the visitor disclosed the receipt of a letter concerning the company'southward failure to comply with NASDAQ listing requirements. Trading of the visitor's shares was halted every bit of the date the complaint was filed, and the company has since been delisted.

Cases Involving Conflicts of Interest

Several cases filed in 2022 allege violations of the securities laws based on a failure to disclose conflicts of interest and significant related party transactions. Many of these purported violations came to lite in connection with the companies' involvement in a transaction that is unrelated to the United States.

For case, in Nancy Lin, et al. v. Liberty Health Sciences Inc., et al., filed in the Southern District of New York, investors brought a securities class action suit confronting the Toronto-based visitor Liberty, whose principal concern activity is the product and distribution of medical cannabis in Florida. The plaintiffs criminate that Liberty violated Sections ten(b) and 20(a) of the Securities Exchange Act of 1934 (the "Exchange Act") by failing to disclose the details of insider transactions, including the acquisition of avails in Latin America via beat entities designed to profit the owners of those entities and an unannounced stock sale which purportedly benefitted insiders at the expense of shareholders.

In Bradley Thomas, et al. 5. China Techfaith Wireless Advice Technology Express, et al., filed in the Eastern District of New York, the plaintiffs allege that "[t]he two brothers who run the Company, Accused Deyou Dong, current Chairman ("Accused Dyou"), and Defendant Defu Dong, former Chairman ("Defendant Defu"), have together caused Communist china TechFaith to engage in undisclosed related party transactions with Defendant Defu'south privately-endemic companies that, over the years, take finer stolen virtually all of the Company'south business organisation and assets and caused the Company's performance to continuously deteriorate and become an unprofitable shell of its erstwhile cocky." "Prc TechFaith's failure to disembalm the material related party transactions . . . violated GAAP, and SEC regulations and rendered Cathay TechFaith'due south fiscal statements simulated and misleading." Investors criminate that when the harm to the visitor's fiscal condition caused by the defendants' fraudulent undisclosed related party transactions was disclosed over fourth dimension, the value of Red china TechFaith shares declined, damaging investors.

In Marker Mikhlin, et al. v. Oasmia Pharmaceutical AB, et al., as well filed in the Eastern Commune of New York, the plaintiffs allege that Swedish biotech company Oasmia violated Sections 10(b) and 20(a) of the Exchange Deed by declining to disembalm the off-the-books related party transactions and outright theft carried out by Oasmia's one-time CEO, Defendant Julian Aleksov, and Defendant Bo Cederstrand, onetime Chairman of the board of Oasmia and a member of Aleksov's family unit.

Some conflicts of interest cases involving transactions were filed in the District of Delaware. For example, in Michael Kent, et al. v. Avon Products, Inc., et al., filed in the Commune of Delaware, the plaintiffs allege violations of Sections 14(a) and 20(a) of the Exchange Act against Defendant Avon Products. The complaint alleges that Avon omitted material information from the proxy statement filed in connectedness with Avon'due south proposed acquisition by Natura Cosmeticos including almost the companies' financial projections; the assay performed by Avon's financial advisors Goldman Sachs and PJT Partners; confidentiality agreements that may have prevented superior conquering offers; and PJT's potential conflicts of interest as a result of having provided by services to Avon, its affiliates and/or Cerberus Capital Management Fifty.P., decision-making shareholder of Avon. The case was voluntarily dismissed on January 22, 2020.

Eric Sabatini, et al. five. Foamix Pharmaceuticals Limited, et al., also was filed in the District of Delaware and alleges violations of Sections 14(a) and 20(a) of the Exchange Human activity. The complaint alleges that Israeli pharmaceutical visitor Foamix omitted material data in its registration statement filed in connection with a proposed merger between Foamix and Menlo Therapeutics Inc. The complaint alleges that the registration statement omits information regarding financial projections, cash-flow analysis and potential conflicts of interest of Foamix's financial adviser, Barclays Banking concern PLC, equally a result of failing to disembalm the amount of compensation Barclays received for by services to Foamix.

Move to Dismiss Decisions

Stoyas 5. Toshiba Corp. et al.

Information technology is worth noting the much-anticipated recent decision past Judge Pregerson in Mark Stoyas 5. Toshiba Corporation et al. in the Central District of California every bit information technology demonstrates that fifty-fifty companies with unsponsored ADRs trading in the United states can be subject to U.S. securities laws.

The defendant in Stoyas is Toshiba Corporation—a "worldwide enterprise that engage[south] in the research development, manufacture, construction, and sale of a broad variety of electronic and energy products and services"— which is headquartered in Japan. The plaintiffs allege that Toshiba violated the Substitution Act as well as Japan'due south Fiscal Instruments & Commutation Deed ("JFIEA"). Toshiba'due south mutual shares trade on the Tokyo stock exchange, simply Toshiba has unsponsored Level I ADRs that trade in the United States (i.eastward., the ADRs were set up past a depositary bank without Toshiba'south involvement). All claims relate to allegations of fraudulent accounting and misrepresentations. The court originally dismissed the get-go amended complaint with prejudice in 2016. The plaintiffs so appealed, and on July 17, 2018, the Ninth Circuit reversed and remanded. Though the Ninth Circuit held that plaintiffs had not sufficiently alleged a domestic transaction nor sufficiently alleged that the fraudulent deport was "in connection with" the sale of securities, the court concluded that leave to amend should take been granted. The U.S. Supreme Court denied certiorari. On August 8, 2019, the plaintiffs filed a second amended complaint, and the defendants moved to dismiss.

This time, Judge Pregerson denied the move to dismiss. The court found that the plaintiffs plausibly alleged that the parties incurred irrevocable liability within the United States, reasoning that allegations regarding the location of the broker, the tasks carried out by the broker, the placement of the purchase order, the passing of title and the payment made were relevant to the domestic transaction enquiry. The court explained, "[t]lid [if] discovery ultimately reveals that the ADR transaction involved an initial purchase of mutual stock in a foreign transaction . . . [that] can be a matter properly raised at the summary judgment stage."

The court also establish that the plaintiffs sufficiently alleged Toshiba's "plausible participation in the establishment of the ADR program." The court stated that the plaintiffs sufficiently declared the "in connectedness with" element of the securities claim. In other words, the plaintiffs alleged "the nature of the . . . ADRs, the OTC market place, the Toshiba ADR program, including the depositary institutions that offering Toshiba ADRs, the Form F-6s, the trading volume, the contractual terms and Toshiba'south plausible consent to the auction of its stock in the United States every bit ADRs." The court likewise institute that the plaintiffs sufficiently alleged that the purported fraudulent conduct curtained the true condition of the visitor and risks associated with its stock. The allegations plausibly demonstrated "some causal connexion" between the defendants' behave and the purchase or sale of the ADRs at event. Terminal, the court ended that the plaintiffs had sufficiently alleged Exchange Act claims, and concluded that comity and forum non conveniens did not compel dismissal.

The ruling shows that fifty-fifty companies with unsponsored ADRs trading in the United States can be discipline to U.S. securities laws, and it is non enough to but defend the matter past arguing that the visitor did not sponsor the ADRs.

Dispositive Decisions of 2022 and 2022 Filings

In 2022 and early 2020, courts issued fewer dispositive decisions on motions to dismiss in securities form actions brought against non-U.S. issuers than were issued in 2022 and early 2019. Specifically, only vii dispositive decisions were rendered. In addition, 4 2022 filings were voluntarily dismissed in their entirety while i 2022 filing was dismissed in its entirety pursuant to a stipulation betwixt the parties. In that location were no dispositive motions to dismiss decisions rendered with respect to 2022 filings, but viii 2022 filings were voluntarily dismissed in their entirety, and one 2022 filing was dismissed in its entirety pursuant to a stipulation between the parties. Finally, the Southern District of New York dismissed, in part, i securities class action that was filed in 2022 and some other that was filed in 2018.

While information technology is difficult to discern trends from just vii dispositive decisions, the courts' reasoning for dismissing cases is nonetheless instructive for not-U.S. issuers who may find themselves subject to securities class action lawsuits.

Commencement, two securities class actions that were brought against non-U.Due south. issuers were dismissed on international comity grounds. In Kim C. Block, et al. v. Interoil Corporation, et al.,51 Gauge Karen Scholer of the Northern District of Texas dismissed a complaint that had been filed against InterOil Corporation, a company headquartered in Singapore and incorporated in Yukon Territory, Canada. In the complaint, lead plaintiff alleges that InterOil circulated simulated information ahead of a shareholder vote regarding whether InterOil should be acquired. The shareholders voted in favor of the acquisition, and the acquisition was subsequently approved by the Supreme Court of Yukon. In addition to challenging the substance of the complaint's allegations, defendants argued that the commune courtroom should not disturb the decision of the Canadian court. Gauge Scholer agreed, explaining:

In the instance at hand, the Court finds that the Canadian courtroom proceedings satisfy every element that warrants dismissal on international comity grounds: (1) the Supreme Courtroom of Yukon was a court of competent jurisdiction that had jurisdiction over InterOil and InterOil's shareholders; (2) the court's last judgment was supported by submissions by InterOil; (three) InterOil shareholders had an opportunity to announced and be heard; (4) the court followed established procedural rules; and (five) the court issued a written order resolving the hearing.

Besides, in EMA GARP Fund, 50.P., et al. v. Banro Corporation, et al., Guess Katherine Failla of the Southern District of New York dismissed a securities class action against Banro Corporation—a visitor that is both incorporated and headquartered in Canada—in deference to a reorganization proceeding in the Ontario Superior Court of Justice that had been ongoing when plaintiffs filed their complaint and in which plaintiffs had elected not to participate. Much like Judge Scholer, Judge Failla explained:

[A]south the [Canadian] [p]roceeding was a parallel proceeding that satisfied fundamental standards of procedural fairness, and every bit dismissal would not violate U.S. law or public policy, the Courtroom exercises its discretion to dismiss Plaintiffs' claims against Banro on international comity grounds.

Judge Failla then went on to dismiss the claims that had been brought against Banro's former CEO, explaining that allowing those claims to continue would "defeat the purpose of granting comity to the Canadian courtroom."

Second, four securities course actions filed in the Southern District of New York against non-U.South. issuers listed on the NYSE or NASDAQ were dismissed in September 2019, each on dissimilar grounds.

In Runcie Dookeran, et al. v. Xunlei Limited, et al., the plaintiffs criminate that Xunlei, a software and engineering science company headquartered in China, and its Main Executive Officer made six materially false and misleading statements post-obit the launch of its OneCoin Rewards Program past failing to disclose to U.S. investors that the program was illegal and banned in Cathay. Approximate Paul Crotty granted defendants' motion to dismiss considering plaintiffs did not allege that the Chinese regulatory authorities accept taken formal activeness against Xunlei with respect to the Programme and did not plausibly allege that, notwithstanding such inaction. Xunlei'southward acquit violates Chinese police force. Moreover, Judge Crotty found that the plaintiffs failed to allege scienter because the regulatory notice regarding the possible illegality was publicly bachelor.

In Rajan Chahal, et al. v. Credit Suisse Group AG, et al., the plaintiffs allege that defendants, listed on the NYSE, made textile misstatements or omissions (1) with respect to the issuance of a complex investment vehicle known as VelocityShares Daily Changed VIX Short Term Exchange Traded Notes and (2) by failing to take action to correct or warn the market during a sudden spike in volatility, as well as engaged in a scheme to dispense the market place past issuing a large volume of boosted notes. Judge Analisa Torres, subsequently considering and rejecting each of the plaintiffs' objections, adopted the magistrate judge'south report and recommendation granting defendants' motility to dismiss in their entirety. The courtroom plant that a supplemental prospectus issued past defendants had expressly warned of all of the material risks involved in purchasing the notes and that the complaint did non support an inference of scienter for either the market manipulation or failure to correct claim.

In Edward Lea, et al. v. TAL Instruction Grouping, et al., the plaintiffs criminate that defendants engaged in two sham transactions, the sale of the company'southward tutoring business and a re-buy of that entity a yr subsequently, and that they made a variety of materially false or misleading statements in connexion with those transactions. Judge Loretta Preska granted defendants' motion to dismiss finding that plaintiffs failed to sufficiently plead that the 2 transactions were fraudulent because they did not properly allege that defendants had control over the target entity. The courtroom reasoned that each allegation of control has "alternative explanations and then obvious that they return plaintiff'southward inferences unreasonable."

In Yongqiu Zhao, et al. v. Deutsche Bank Aktiengesellschaft, et al.,58 the plaintiffs allege that Deutsche Bank'south statements that its internal command over fiscal reporting was effective based on the Committee of Sponsoring Organizations of the Treadway Committee ("COSO") framework were fraudulently and materially misleading based on concerns with the Bank's business raised by the Wall Street Periodical. Gauge Alison Nathan granted defendants' motility to dismiss with prejudice finding the allegations to exist conclusory because the plaintiffs did non plead how whatever of the supposed deficiencies in the bank's controls may have led to bug with its financial reporting.

Finally, in January 2020, the Southern District of New York dismissed a securities form action that was brought against Telefonaktiebolaget LM Ericsson—a company headquartered and incorporated in Sweden that trades on the NASDAQ. In Bristol Canton Retirement System, et al. five. Telefonaktiebolaget LM Ericsson, et al., the plaintiffs allege that Ericsson "misrepresent[ed] Ericsson's true financial condition by inaccurately accounting for its long-term contracts and past making fake statements regarding those contracts." Specifically, plaintiffs allege that the visitor engaged in 4 types of business/accounting practices that information technology did not disembalm:

- inbound into negative-value contracts;

- entering into contracts in which project scope exceeded the "fixed price" found on the contracts;

- pushing costs to futurity quarters; and

- prematurely recognizing revenue.

Of note, the plaintiffs allege that the decision to enter into the negative-value contracts "was made past Swedish headquarters." Approximate Jesse Furman granted the defendants' motion to dismiss explaining, inter alia, that plaintiffs had failed to criminate that the defendants' statements regarding public statements were false in light of the 4 practices alleged, and that even if the plaintiffs had alleged the falsity of those statements, the plaintiffs had failed to allege that those statements were made with the requisite scienter.

Conclusion

A company does not demand to be a U.S. issuer to face potential securities class action liability in the United States. Instead, as the foregoing analysis demonstrates, non-U.S. issuers remain targets of securities class activity suits even when the alleged actions occurred abroad and even with unsponsored ADRs trading in the United States. As such, it is imperative that not-U.S. issuers take steps to mitigate risks in not but their domicile jurisdictions merely also in the United states of america.

Non-U.S. issuers should be especially cognizant when making disclosures or statements to:

- speak truthfully and to disclose both positive and negative results;

- ensure that a disclosure regimen and processes are well-documented and consistently followed;

- work with counsel to ensure that a disclosure plan is adopted that covers disclosures made in printing releases, SEC filings and by executives; and

- understand that companies are not immune to problems that may cutting across all industries.

Non-U.South. issuers should work with the company's insurers and rent experienced counsel who specialize in and defend securities course action litigation on a total-time basis. Finally, to the extent that a not-U.S. issuer—despite its diligent mitigation efforts—finds itself the subject of a securities class action lawsuit, the bases upon which courts accept dismissed similar complaints in the past tin can exist instructive.

The consummate publication, including footnotes, is available here.

Source: https://corpgov.law.harvard.edu/2020/03/29/non-u-s-issuers-targeted-in-securities-class-action-lawsuits-filed-in-the-united-states/

0 Response to "Class Action Lawsuit Again a Foreign Company"

Post a Comment